Housing Market Snapshot - New England North West Region

The Housing story in New England North West

The New England North West region is comprised of the twelve local government areas of Armidale Regional, Glen Innes Severn, Gunnedah, Gwydir, Inverell, Liverpool Plains, Moree Plains, Narrabri, Tamworth Regional, Tenterfield, Uralla and Walcha.This region includes the major centres of Tamworth and Armidale as well as the key centres of Gunnedah, Glen Innes, Inverell, Moree and Narrabri.

Infrastructure Australia’s report “2022 Regional Strengths and Infrastructure Gaps” notes that the Regions’ natural environments encompass national parks, wetlands, forests, bushlands, tablelands, rivers, and plains and that the region has experienced increasingly frequent extreme weather events, including bushfires, droughts, and floods. The report adds that the region has seen diversification of industry, with value-add agricultural products from food manufacturing and renewable energy generation being most prominent. In addition, the region is home to a strong knowledge sector and master planning for the Narrabri Special Activation Precinct is underway.

Like NSW generally, the New England North West has had a low vacancy rate for some time, indicating a tight rental market due to lack of supply and impacting access to, as well as affordability of private rental. While this region is more affordable for rent and purchase than coastal areas of NSW, rents are rising here too and there are increasing numbers of rental households in stress. There is also a lack of diversity in the housing stock.

What’s the housing demand?

Between 2016 and 2021, the population of the New England North West grew by 2.2%. This overall growth for the region masks significant differences in the experience of population change in individual LGAs within the region. Gwydir, Liverpool Plains, Moree Plains, Narrabri, Uralla and Walcha all experienced a loss of population over this period, while all the remaining LGAs in the region saw population growth.

As a region, New England North West has a higher proportion of 0--34 year olds than the Rest of NSW average and lower proportions of older age groups. However, not every LGA in the region follows this pattern. Generally, Glen Innes Severn, Gwydir, Liverpool Plains, Tenterfield, Uralla and Walcha have higher proportions of cohorts aged over 55 years than the Rest of NSW average. While Armidale Regional, Gunnedah, Inverell, Moree Plains, Narrabri and Tamworth Regional tend to have higher proportions of cohorts under 35 years than the Rest of NSW average.

All the New England North West LGAs have higher proportions of other household types (which include multi-family households) than the Rest of NSW. For the New England North West region as a whole, lone person households are the largest household type (27.0%) along with couple families without children (26.5%). Given the predominance of lone person and couple only households and that there has also been an increase in smaller household types since 2016, it suggests the need for an increasing diversity of bedroom mix, including more studio (bedsit), one and two bedroom homes to suit different household types. The high proportions of “other household” types underlines the need for more homes with a larger number of bedrooms.

Low income households comprise the largest proportion of all households in the New England North West. Across the region the number of low income households increased by 14.3% between 2016 and 2021, while moderate income households increased by 3.2% and high income households declined by -14.2%. The predominance of, as well as increase in low income households implies increasing demand for affordable rental and purchase.

What’s happening in the market?

Housing market conditions and rent and purchase affordability varies significantly within the region, particularly between the larger centres, mining communities and the rest of the region. With a tight rental market and declining numbers of affordable rental properties, there are higher numbers of lower income rental households in housing stress.

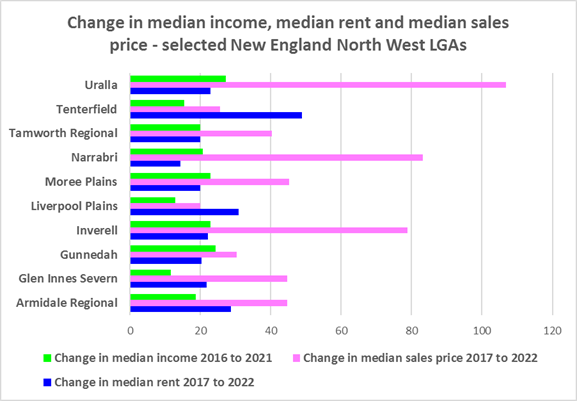

Looking at median rents for all residential dwellings combined together, there have been strong increases in the New England North West region since 2003, with some variability between 2019 and 2022, due to the pandemic.

The LGAs of the New England North West are more affordable for rent by very low and low income households than the average for the Rest of NSW. However, within the region the average proportion of very low income households in rental stress at 2021 was 87.1%, with the proportion varying from 90.5% in Armidale Regional to 70.1% in Gwydir. 53.4% of low income households were in rental stress on average for the region, varying between 58.6% in Gunnedah and 30.3% in Gwydir. The proportion of very low and low income households in rental stress has increased from 2016. At the same time there has been a decline in the number of rental bonds lodged that are affordable to lower income households – indicating a reduction in supply of affordable private rental.

The long term median sales price trend shows growth across all LGAs in the region. Just in the 12 month period between March 2021 and March 2022, median sales prices increased strongly in every LGA (except Moree Plains) – with rises of 53.4% in Narrabri, 51.1% in Uralla, 43.6% in Liverpool Plains and 41.9% in Gunnedah. Purchase affordability for very low and low income households is significantly better than the average for the Rest of NSW in all the New England North West LGAs and consequently the proportion of very low and low income households in purchase stress is much lower than the Rest of NSW average.

The number of very low and low income renters in housing stress is much greater than the number of very low and low income purchasers in stress in New England North West.

What’s happening with supply – and is it a good match?

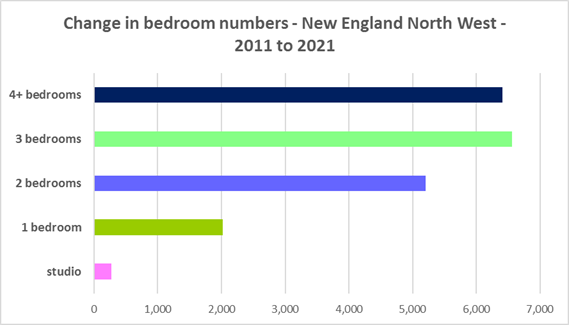

The majority of households in the New England North West are couple or single person households, yet the housing stock is primarily comprised of three or four bedroom detached homes. At the same time, there are significant numbers of “other households” - which include multi- family households – in the region, potentially signalling a demand for larger homes as well. It could also signal an affordability issue.

Separate houses comprise 89.2% of all occupied dwellings, above the average of 82.5% in the Rest of NSW. More importantly, across the region 42.2% of dwellings have three bedrooms and a further 36.0% have four or more bedrooms. Only 0.5% of homes are studios, 3.8% have one bedroom and 15.4% have two bedrooms. Given that lone person and couple only households comprised 49.4% of all households in the New England North West, the fact that studio and one bedroom homes combined comprise just 4.3% of the housing stock shows a mismatch between household type and dwelling size and a significant lack of housing choice for smaller households.

The forecast increase in older age groups in the region is likely to increase the demand for smaller, more manageable and affordable homes. It is important for older residents to be able to downsize from larger family dwellings to smaller homes that are easier to manage and maintain, to assist them to retain their independence. Two bedroom dwellings in particular offer the most flexibility, given they are also suitable for small families and allow older residents to have family members or carers to stay.

In addition to more diverse housing supply, particularly for smaller households, there is a need for more affordable rental housing for lower income households, as well as for increasing numbers of seniors and frail aged.

Secondary dwellings and new generation boarding houses would help meet some of the demand for smaller rental dwellings for single people and couples, for lower paid workers and students. Affordable rental housing for students is clearly an issue in Armidale Regional. New generation boarding houses have potential to assist in providing student accommodation as well as housing for seasonal workers and mine workers. Partnering with a community housing provider has the most potential for increasing affordable rental housing supply.

Change 2016 to 2021

Comparative stats

- Population at 2021: 185,619

- Number of dwellings at 2021: 78,398

- Number of households at 2021: 76,173

- Number of rental households at 2021: 20,563

- The number of Very Low and Low income households at 2021: 38,021

- Number of Very Low and Low income rental households at 2021: 7,966

- Number of Very Low and Low Income Renters in Housing Stress at 2021: 5,314

- Reduction in new rental bonds lodged affordable to low income households (2017-2021): -17.8%

- Number of new rental bonds lodged affordable for low income households 2022: 1,230

- Number of Homeless at 2021: 570

- Number of Marginally Housed at 2021: 560

Key regional stats

- Number of lone person households: 20,588

- Number of couple only households: 20,241

- Number of studio dwellings: 362

- Number of one bedroom dwellings: 2,617

- Number of caravan, cabin, houseboat and improvised dwellings: 360

- Number of unoccupied dwellings: 9,481

Additional information

Additional information on:

What’s happening with demand is at